All Things 401(k): Types of Fiduciaries and Minimizing Liability

If you are a plan sponsor of a retirement plan, I’m sure you have heard of the term “fiduciary”. If you are thinking about starting a retirement plan for your company, this is a term you should be aware of, become familiar with, and understand what it means.

What is a Fiduciary?

Let’s start off with explaining what a fiduciary is. Fred Reish published an article called What Is a 401(k) Fiduciary And Why Does It Matter? that explains what a 401(k) fiduciary does, as “A fiduciary is responsible for running the plan. The person, or group of people, who make decisions about plans and their investments are fiduciaries. They must act prudently and in the best interest of the employees. Prudence means that they have to make decisions carefully and thoughtfully.”

Fiduciary Responsibilities

It is important to designate the right person within an organization to take on the fiduciary title, but to also understand the responsibility and liability that comes along with it. The IRS explains Retirement Plan Fiduciary Responsibilities include:

• “acting solely in the interest of the participants and their beneficiaries;

• acting for the exclusive purpose of providing benefits to workers participating in the plan

and their beneficiaries, and defraying reasonable expenses of the plan;

• carrying out duties with the care, skill, prudence and diligence of a prudent person familiar with the matters;

• following the plan documents; and

• diversifying plan investments.”

All in all, a fiduciary must do what is in the best interest of the organization’s plan participants. This may seem overwhelming if you are reading these responsibilities and thinking to yourself – What are reasonable expenses for a 401(k) plan? How do I understand what the plan document means and how do I follow it? I’m not an expert on investing – how do I diversify plan investments?

Outsourcing Fiduciary Liability

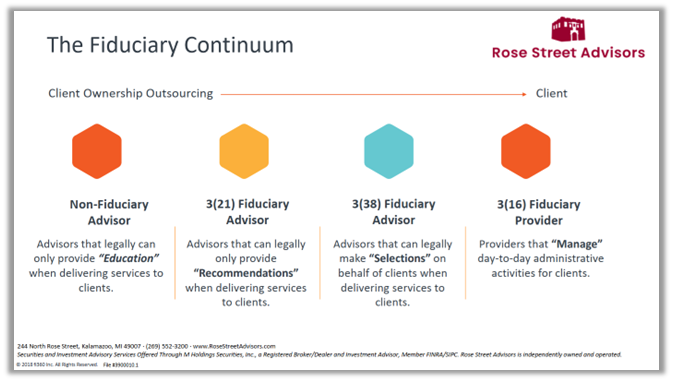

This is where fiduciary advisors/providers come into play. There are ways to minimize fiduciary liability by outsourcing certain fiduciary responsibilities. As an HR professional or owner of a company, there are specialties/expertise that you have in your role. You are not expected to be an expert on the fiduciary duties of managing a 401(k) plan but to educate yourself and reduce liability where needed. There are people and/or companies out there that specialize in specific areas of fiduciary duties. Through my Accredited Investment Fiduciary (AIF®) Training through Fi360 A Broadridge Company, they shared an illustration of what we call the Fiduciary Continuum.

The Fiduciary Continuum shows different types of advisors that can provide education only, provide recommendations, make investment selections on your behalf, and certain providers will even manage day-to-day administration for clients. When implementing a new 401(k) plan for an organization, you will likely need an advisor to consult on how to set up the plan and give recommendations on multiple aspects such as plan design, investment selection, understanding legal plan documents, etc.

Types of Fiduciary Advisors/Providers

Depending on the Financial Advisor that you work with, a non-fiduciary advisor can legally only provide education to clients. This type of Financial Advisor is not a fiduciary and is not held to the same standard as a Fiduciary Advisor. In this scenario, the advisor is not required to avoid or disclose potential conflicts of interest. Often, this relationship pays the advisor a commission based on transactions, or they can get paid by the products that they sell.

A 3(21) Fiduciary Advisor is an investment advisor that provides investment recommendations and is a co-fiduciary on the plan. This means that they can assist in creating the investment lineup for the plan, monitor the performance of the investments, and make recommendations. Hiring a 3(21) Fiduciary Advisor would make sense if you are knowledgeable about investments and have the time to monitor the plans investments. In addition to that, you would prefer to actively manage the plans investments and be open to recommendations from the advisor, but also understand that you are liable for monitoring investment fees and performance of the plan.

A 3(38) Fiduciary Advisor is a little different in that they, manage the investments in the plan. This means that they make the decisions of creating the plan lineup, implementing the plan lineup, monitoring the investments, and making changes as necessary. Hiring a 3(38) advisor would be suitable if you are too busy for the extra responsibility of making investment decisions on the plan, are not knowledgeable about investment management, or want to put more of your efforts into running your business rather than the plan. You can delegate the investment management to an experienced advisor and reduce your fiduciary liability.

The last piece in the Fiduciary Continuum, is a 3(16) provider which is usually a Recordkeeper that would provide this service. You may also hear this referred to as a 3(16) Plan Administrator. This type of Fiduciary Provider essentially takes over plan administration duties from the plan sponsor. This reduces liability even further by taking on a laundry list of responsibilities regarding the administration of a 401(k) plan. A few examples of these responsibilities include, reviewing and signing the Form 5500, approving and rejecting withdrawals and loans in accordance with the plan document, fixing compliance errors, and tracking and communicating participant eligibility. This would delegate administrative duties and minimize your fiduciary liability even further. This can be used in addition to the 3(21) Fiduciary Advisor or 3(38) Fiduciary Advisor as well to take a significant amount of liability off of the plan sponsor.

Selecting a Fiduciary Advisor

It’s important to ask certain questions when selecting an advisor to ensure that they have the fiduciary knowledge and tools needed to provide services in the best interest of their clients. Below are some questions you can ask, that your advisor should be able to clearly answer and are able to disclose the information to you in writing:

1. Will you act as a fiduciary in all situations when managing plan assets and/or participant portfolios?

2. What fiduciary training have you received?

3. Do you hold any designations focused on fiduciary best practices?

4. What services do you provide to help your clients meet their fiduciary obligations?

5. Do you offer any fiduciary services that can reduce my fiduciary liability?

6. Are there any potential conflicts of interest?

7. How will you be paid for the proposed services?

Once you have clear answers and disclosures of these different aspects, you will be in a better position to evaluate if the advisor and/or provider is a good fit. Ask more questions to determine which fiduciary responsibilities you will take on as the plan sponsor and which you will outsource. Speaking with a trained fiduciary advisor should feel like a partnership or an extension of your team, that you can lean on when you have questions or concerns. They will be able to advise on other ways to minimize your fiduciary liability and help make sure your plan is managed effectively and in line with laws and regulations. Ask the questions and remember to make decisions carefully and thoughtfully.

JULIA MUNSON

AIF® | Retirement Relationship Manager

Meet Julia, a people-focused life-long learner with several years of experience in the retirement plan industry. Throughout her career, Julia has been committed to maintaining strong client relationships by providing incredible customer service. She is passionate about helping clients define and plan for their retirement goals. Julia’s daily role at the firm energizes and reinforces her commitment to client-focused work.

This material and the opinions voiced are for general information only and are not intended to provide specific advice or recommendations for any individual or entity. To determine what is appropriate for you, please contact your Rose Street Financial Professional. Information obtained from third-party sources are believed to be reliable but not guaranteed.

Investments in securities involve risks, including the possible loss of principal. When redeemed, shares may be worth more or less than their original value.

By accessing any links above, you will be connected to third party web sites. Please note that Rose Street Advisors, LLC, is not responsible for the information, content or product(s) found on third party web sites.

Securities and Investment Advisory Services Offered Through M Holdings Securities, Inc. A Registered Broker/Dealer and Investment Adviser, Member FINRA/SIPC. Rose Street Advisors, LLC is independently owned and operated. File #: 5450988.1

Interested in more?

Securities and Investment Advisory Services Offered Through M Holdings Securities, Inc. A Registered Broker/Dealer and Investment Advisor, Member FINRA/SIPC. Rose Street Advisors is independently owned and operated.

Please go to www.mfin.com/DisclosureStatement for further details regarding this relationship.

Check the background of this Firm and/or investment professional on FINRA’s BrokerCheck.

For important information related to M Securities, refer to the M Securities’ Client Relationship Summary (Form CRS) by navigating to mfin.com/m-securities

Registered Representatives are registered to conduct securities business and licensed to conduct insurance business in limited states. Response to, or contact with, residents of other states will only be made upon compliance with applicable licensing and registration requirements. The information in this website is for U.S. residents only and does not constitute an offer to sell, or a solicitation of an offer to purchase brokerage services to persons outside of the United States.

This site is for information purposes and should not be construed as legal or tax advice and is not intended to replace the advice of a qualified attorney, financial or tax advisor or plan provider. CA Insurance License. File #5757992.1